Wed, Jul 27, 2016

Cost of Capital Considerations of Brexit

The webcast focused on the challenges of estimating the cost of capital from the perspectives of U.S., UK, and Eurozone investors in a post-Brexit world. This article is a follow-up to the issues discussed during the webinar.

Immediately following the June 23, 2016 vote by the UK electorate to leave the European Union (EU), shockwaves were sent to global financial markets. The initial state of panic was ensued in the weeks that followed by a recovery in certain market indicators.

Yet, the aftermath of the Brexit vote is still characterized by significant signs of uncertainty, which is weighing on investors. Almost a month after the vote:

-

The Pound Sterling (GBP) is still down by about 10% relative to the U.S. dollar (USD) and the euro (EUR)

-

The FTSE 250 (in GBP) (companies generating a higher proportion of revenues from the UK), STOXX Europe 600 (in EUR), and the Euro STOXX Index remained below pre-Brexit vote levels

Pockets of investors continued to look for safety:

-

Gold prices increased in the weeks following the vote, although they seem to have recently stabilized

-

The yields on U.S. 10-year Treasury bonds and UK 10-year Gilts plunged to record lows

-

The yield on German 10-year Bunds turned negative for the first time

For perspective, in relative terms the UK, 10-year yield declined by almost 50% in the space of just three weeks, whereas the German 10-year yield fell threefold from its original level on Brexit vote day.

Commentators noted initially that the dramatic declines following the Brexit vote were caused by “flights to quality”– investors seeking to preserve the principal of their investments given the increased risks. Since then, continued investment demand for safe-haven bonds is also driven by investors’ expectations that major central banks around the world will implement new (or expand existing) quantitative easing (QE) policies, thereby supporting bond prices for the foreseeable future.

In addition, global expectations of long-term growth have been abating since the onset of the global financial crisis in 2008, which along with a low-inflation (or even deflationary) environment, suggest that nominal investment returns for equity securities may fall well-short of those realized over prior decades.

The remainder of this article will discuss issues confronting investors in valuing their investments in the current environment. We will use June 30, 2016 as a reference date.

Recall that the value of any investment is a function of three key inputs: (i) expected cash flows from existing investments, (ii) expected growth in earnings and cash flows, and (iii) the required rate of return (discount rate) to convert the expected cash flows into their present value.

Expected Growth in Net Cash Flows

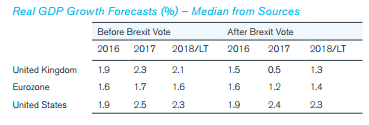

We first discuss the impact of the Brexit vote on the expected growth in earnings and cash flows. We assembled data on the expected growth of real Gross Domestic Product (GDP) prepared before and after the Brexit vote by a variety of reputable sources.1

The following table summarizes the changes in projected real GDP growth (the median of projections) for 2016, 2017 and 2018 or long-term (LT):

As one would expect, the UK is expected to suffer the largest negative impact (with a median 80% decline in 2017 real growth), followed by the Eurozone, with the U.S. expected to be minimally affected.

This significant deterioration of growth expectations will have a negative effect on many investments. Analysts should consider measuring exposure of individual investments to the UK and the Eurozone, and revising their projected cash flows accordingly. But how? The analyst needs to carefully evaluate the sources from where revenues and costs are generated, in order to quantify how the changes in real GDP growth will impact the subject company’s expected cash flows. For example, large UK publicly-traded companies (in the FTSE 100) only generate about 20% of their revenue from the UK, while smaller mid-cap public UK companies (in the FTSE 250) generate about 50%.2

Discount Rate

Recall that the cost of equity (COE) capital is typically expressed as a function of the risk-free rate and the equity risk premium (ERP). A base COE can be obtained by adding the risk-free rate to the ERP.

-

Building Blocks of Cost of Equity Capital

-

Risk-Free Rate

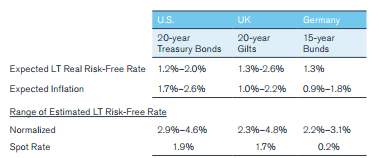

As indicated earlier, the yields on U.S. Treasury bonds, UK Gilts, and German Bunds – three of the most-commonly used proxies for the risk-free rate – all declined precipitously following the Brexit vote. The currently record-low interest rates are being driven primarily by (1) QE policies of major central banks; (2) “flights-to-quality”; and (3) declining expectations for real growth rates and inflation.

We examined what one could expect the risk-free rate to be absent central bank interventions and flights-to-quality. Corporate finance theory tells us that nominal long-term interest rates should reflect: (i) real rate of return (time value of money), (ii) inflation expectations and the risk of changes in inflation, and (iii) maturity risk. We assembled data from various sources for three bonds commonly used as inputs to COE, comparing the estimated normalized rates relative to the spot rates as of June 30, 2016 (note that spot yields have declined even further since then):

How should the analyst use this information? One can calculate the COE by either starting with a normalized risk-free rate or a spot rate. However, it’s critical to match the second building block, the estimated ERP, to the selected risk-free rate. There must be internal consistency between these two inputs: building blocks of Cost of Equity Capital; and Risk-Free Rate.

Recall that the ERP is the difference between the expected rate of return on a fully-diversified portfolio of stocks and the expected rate of return on the risk-free security.

If one uses a spot rate artificially kept low by actions of central banks and flights-to-quality, but continues to use a long-term average historical ERP to calculate the base COE, one may end up with nonsensical results.

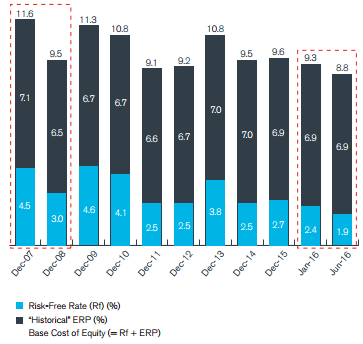

The need for internal consistency is illustrated in the following example. The long-term historical realized ERP since 1926 based on the S&P 500 is a common source of ERP estimates.3 Let us examine the results for December 31, 2007 and 2008:

Just when risks to investors were at all-time highs, this commonly-used method resulted in a nonsensical decrease in the base COE (from 11.6% to 9.5%). A similar pattern emerged at June 30, 2016, with this method implying a decline in base COE to 8.8%. The analyst must then ask: did the risks in the future cash flows really decline? If not, then the ERP must have increased, such that the base COE remains approximately the same.

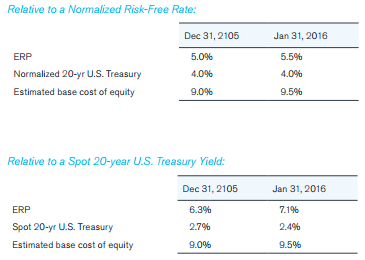

Duff & Phelps examines a variety of economic and financial market indicators each month, in order to estimate a recommended ERP, which is expressed relative to a normalized risk-free rate. This ERP estimate can be converted into a premium relative to the spot risk-free rate. For example, as of December 31, 2015 and January 31, 2016 we reported the following recommended base cost of capital inputs for U.S. companies with cash flows estimated in USD4:

As of June 30, 2016, when markets had begun to settle down, our analysis indicated that for investments with cash flows denominated in USD, the recommended ERP as of January 31, 2016 should continue to be used.

Conclusion

Matching expected return to risk remains an inexact exercise. It is critical to maintain internal consistency between assumptions, when conducting a valuation. One must estimate growth in cash flows consistent with current expectations. And in discounting those expected net cash flows, one must use an expected base COE that matches expected return to the expected risks.

Notes:

Webinar speakers included professors Aswath Damodaran (NYU Stern School of Business), Elroy Dimson, (Judge Business School, University of Cambridge) and Pablo Fernández (IESE Business School), as well as Kroll managing directors Roger Grabowski and Yann Magnan.

View the Webcast Replay

1.Moody’s Analytics, Standard & Poor’s, IHS Global, Consensus Economics, The Economist Intelligence Unit, Oxford Economics, and IMF (the latter, for the UK and Eurozone only)

2.Michael Hunter, “UK’s FTSE 250 has more to worry about than Brexit”, FT.com, May 26, 2016

3.As reported before 2014 in the SBBI Valuation and Classic Yearbooks and since 2014 in the Kroll Valuation Handbook – Guide to Cost of Capital

4.2016 Valuation Handbook – Guide to Cost of Capital, Chapter 3

Valuation Advisory Services

Our valuation experts provide valuation services for financial reporting, tax, investment and risk management purposes.

Business Valuation Services

Kroll is the largest independent provider of business valuation services.