As the election in Brazil approaches, political uncertainty may slow investment activity in the second half of 2018. Questions about who will lead the country has led many investors to delay closings until post-election in October.

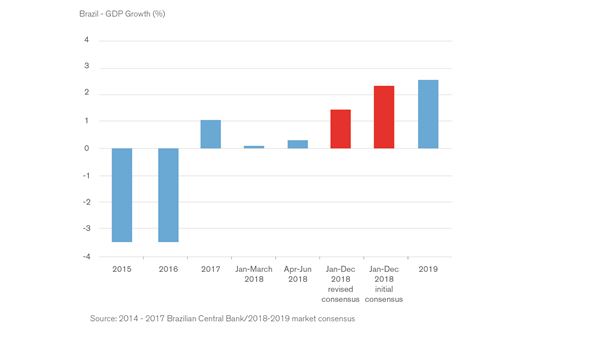

Besides the election, a number of unexpected socioeconomic events have affected Brazil’s gross domestic product (GDP), which grew at a slower pace than expected for the first half of the year. GDP for 2018 was initially predicted at 2.3% but is now closer to 1.5%, according to a Central Bank report. The change is attributed to the truckers’ strike in May, higher than expected inflation, continuing high unemployment rate (at 12.3%, according to IBGE), a persistent fiscal deficit and high government debt (at 77% of GDP, according to the Central Bank) and the interruption of the voting in Congress.

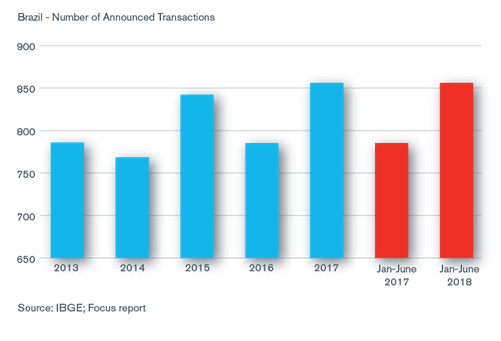

Despite these factors, M&A activity in Brazil has gained momentum. In the first half of 2018, M&A activity grew 18% compared to the same period in 2017, with 471 transactions announced and a total value of R$ 101 billion (US$ 28 billion), according to Fusões & Aquisições. Driving this are lower interest rates (the basic rate is at a record low of 6.5% per year) and a depreciated Real against the Dollar (a trend observed worldwide, where the Dollar has strengthened). As a result, Brazilian assets are very attractive propositions in terms of purchase price and many buyout opportunities are being explored. But in the second half of the year, business in general is awaiting the outcome of the election before making important decisions – a behavior that is holding back M&A transactions.

The deal flow would have been even more robust if there were no disagreement between buyers and sellers, particularly on target company valuations (driven mainly by different points of view on short and mid-term perspectives and projected risk). Sellers are asking higher prices, expecting the same value as those seen prior to Brazil’s recent economic crisis. However, buyers are not in a position to pay.

According to Transactional Track Record, technology was the most active sector in the first half of 2018, followed by financial services. The same report concludes that transactions involving venture capital funds increased 23% compared to the first half of 2017, showing an increased appetite for riskier assets even in a less-than-favorable economy.

Private equity investment remains strong, with fund managers expecting to raise between US$ 3.5 billion and US$ 3.7 billion in 2018 for their funds in Brazil, which Valor Econômico reports as the highest level since 2014. Although the domestic environment for raising capital is challenging, international investors continue to have an appetite for Brazilian investments.

Despite growth in some sectors, Brazil is below target investment rates. According to IBGE, Brazil has investment rates of about 15% of GDP, where it should be targeting 20%. A well-structured and ambitious program of privatization and concessions is one way to attract investments, strengthen growth and reduce unemployment. Brazil’s investment needs will likely be funded privately, as the government is unable to satisfy the demand for funds.

Capital markets will also play a decisive role in Brazilian investment and development. According to an Accenture Strategy study, a stable growth scenario of 2% to 3% per year and an active capital market could bring Brazil an additional R$ 300 billion in funds and infrastructure investments from 2018 to 2022. This could generate an additional 1.7 million jobs and increase average per capita income about 12% in a period of four years.

Looking further ahead, M&A activity will likely increase over the next few years as investments are made to improve Brazil’s infrastructure deficits in healthcare and education (mainly in K–12, EdTechs and corporate training). In healthcare, which is overall still regional and fragmented, there are many opportunities for consolidation.

Renewable energy and real estate may continue to be M&A hot spots. Brazil’s natural resources, specifically wind power, and the increasing demand for energy have heightened interest in the sector. Low property prices, in addition to favorable foreign exchange rates and low local interest rates, have created opportunities for real estate investors.

Investments in the country will likely be maintained by investors who are already acquainted with Brazil’s intricate deal environment and economy. According to a report published by Saint Paul Escola de Negócios and the Brazilian Institute of Finance Executives, CFO levels of confidence remain high (at 130 points) after sinking to levels below 100 points in the first and second quarters of 2016. The report notes that companies are holding on to investments but have market confidence and cash for expansion and M&A activity when the right opportunities arise.

Driving near- and long-term activity in Brazil will continue to be speculation over the political outcome. The market expect that the next president will succeed in gaining approval on important structural reforms (priority should be the pension reform), reducing the government’s fiscal deficit and creating a sustainable framework for increased economic activity and investments.

Corporate Finance and Restructuring

M&A advisory, restructuring and insolvency, debt advisory, strategic alternatives, transaction diligence and independent financial opinions.

Mergers and Acquisitions (M&A) Advisory

Kroll’s investment banking practice has extensive experience in M&A deal strategy and structuring, capital raising, transaction advisory services and financial sponsor coverage.

Transaction Advisory Services

Kroll’s Transaction Advisory Services platform offers corporate and financial investors with deep accounting and technical expertise, commercial knowledge, industry insight and seamless analytical services throughout the deal continuum.

Fairness and Solvency Opinions

Duff & Phelps Opinions is a global leader in Fairness Opinions and Special Committee Advisory, ranking #1 for total number of fairness opinions in the U.S., EMEA (Europe, the Middle East and Africa), Australia and Globally in 2023 according to LSEG (FKA Refinitiv).

Financial Sponsors Group

Dedicated coverage and access to M&A deal-flow for financial sponsors.

Distressed M&A and Special Situations

Kroll professionals have advised hundreds of companies, investors and other stakeholders at all stages of distressed transactions and special situations.

Private Capital Markets – Debt Advisory

Kroll has extensive experience raising capital for middle-market companies to support a wide range of transactions.