The world economy is gradually recovering from the recession inflicted by the COVID-19 pandemic in the course of 2020. The pandemic itself is still here, of course, causing continuing damage and massive uncertainty. Contagion remains widespread and there are growing fears about new variants which could turn out to be more dangerous and/or difficult to contain. But massive vaccination campaigns are now being pursued in an increasing number of countries and vaccine shortages should soon be overcome, at least in the developed world. There are, however, huge divergences across the globe. At one end are several small countries, mainly in the Middle East (e.g. Israel or the UAE) where the bulk of the population has already been vaccinated. In between stand two major economies, the UK and the U.S., where vaccines have been administered to a third or more of the population. At the other end, unfortunately, are a very large number of countries in which vaccination campaigns have hardly begun.

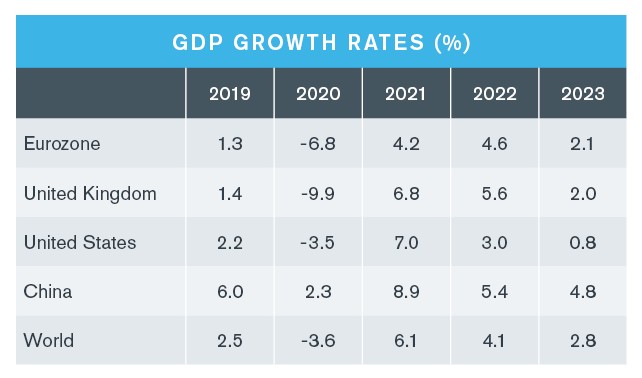

The economic divergences are not as acute, but 2020 estimates and 2021 forecasts show significant differences in performance. 40 per cent of the world economy may record a cumulative GDP growth rate of close to 4 per cent over these two years; but this growing 40 per cent is made up of just two economies: the U.S. and China, accounting for not quite 25 per cent of the world’s population. The remaining 60 per cent, or nearly 200 countries and three quarters of the world’s population, may grow by, at most, 1 per cent from 2019 to 2021.

Both the U.S. and China seem to have coped rather successfully (in relative terms) with the economic consequences of the pandemic. In the U.S. this is mainly due to policy (though having a flexible economy has also helped). Fiscal policy, in particular, now that the $1.9 trillion American Rescue Plan promoted by President Biden has been signed into law, is pumping something like 20 per cent of GDP into the economy over 2020-21. This is leading to a likely boom in activity. In China, the so far rather efficient containment of the pandemic has allowed the underlying dynamism of the economy to reaffirm itself, with policy, if anything, playing a restraining role. As a consequence, growth this year could reach 7 and 9 per cent respectively in the two countries, with GDP at end-year well above its end-2019 levels.

In the emerging world (excluding China), the outlook is much less promising. There are exceptions, of course, India being a notable one. After a sharp drop in output in 2020, the country is expected to more than make up the lost ground this year, with an expected growth of 10 per cent or more. There are some other high performers, especially in East Asia (e.g. Indonesia, Taiwan or Vietnam) and in Eastern Europe (e.g. Hungary, Poland or Romania). But the Latin American picture looks dismal. COVID-19 related death rates were high in many countries. The three largest economies (Brazil, Mexico and Argentina) are only seeing muted recoveries this year and the same will be true for Argentina next year as well. Similarly, Sub-Saharan Africa’s three largest economies (Nigeria, South Africa and Angola) are unlikely to record much growth between 2019 and 2022.

The picture in the developed world outside the U.S. is not very encouraging either. The Eurozone and Japan are stuck in a low growth environment, unable this year to fully offset the sharp drops in output recorded in 2020. Return to 2019 levels of activity will have to wait for the end of 2022, if not 2023. Slow or almost non-existent (as in Japan) vaccination campaigns are one reason for this. Much more timid policies, particularly on the fiscal front (when compared to the U.S.) are another. The UK picture is somewhat stronger, thanks to a rather successful mass vaccination effort and to a robust fiscal response but is negatively influenced by the many costs which Brexit is inflicting on the economy.

Recent indicators for Western Europe suggest that the manufacturing sector at least is showing signs of relatively rapid recovery, pulled up by American and Chinese demand, in sharp contrast to the more sluggish service sector. This, in turn, is likely to favour Northern European countries (such as Germany or Sweden) at the expense of the more tourist dependent economies of the South (such as Italy, Spain or Greece). All forecasts for Continental Europe are, however, clouded by the uncertainties surrounding the unfolding of the vaccination campaigns and the spread of COVID-19. Any strengthening of the disease accompanied by renewed lockdowns and travel bans would, inevitably, hit tourist-dependent economies more than proportionately. Policies remain accommodating, but there are limits to the potential generosity of fiscal policy, limits which are being gradually approached in a number of countries. On the plus side, growth should be helped by the expansionary measures taken in the U.S. and by the likely unwinding of the sharp rise in household savings recorded almost everywhere during the lockdown period.

Fears have been expressed that this pent-up demand could generate renewed inflationary pressures. Inflation is indeed likely to rise this year, but only modestly. And a good deal of this upward spurt will reflect one-off factors such as the reversal of VAT cuts or temporary rises in raw material prices. For higher inflation to entrench itself would require rapid increases in wages. These look very unlikely given that unemployment rates are expected to remain relatively high almost everywhere.

The last article mentioned the unexpected resilience of the real estate sector in most European countries in the course of 2020. Despite recording the worst recession ever since data on GDP exist, house prices rose virtually everywhere in Western Europe in the course of the year. One obvious reason for this was the very low level of interest rates. Another was banks’ willingness to lend funds for house purchases: the growth of mortgage lending in the Euro area in 2020 was the highest since 2008. In addition, the falling supply of new housing may also have had an influence. Residential construction fell, at times quite sharply, across Western Europe (Germany and Sweden being the main exceptions). Easy finance, declining supply and continuing demand, consequent in part on changes in housing preferences due to the pandemic, have all made for price resilience. This may, however, not continue as housebuilding recovers this year and banks rein in their lending.

Source: Oxford Economics

Source: Oxford Economics

By Professor Andrea Boltho, Duff & Phelps Real Estate Advisory Group (REAG) Advisory Board Member, Emeritus Fellow, Magdalen College, University of Oxford.

Valuation Advisory Services

Our valuation experts provide valuation services for financial reporting, tax, investment and risk management purposes.

Real Estate Advisory Group

Leading provider of real estate valuation and consulting for investments and transactions.