This article was contributed by Andrea Boltho, Duff & Phelps Real Estate Advisory Group (REAG) Advisory Board Member and Emeritus Fellow, Magdalen College, University of Oxford.

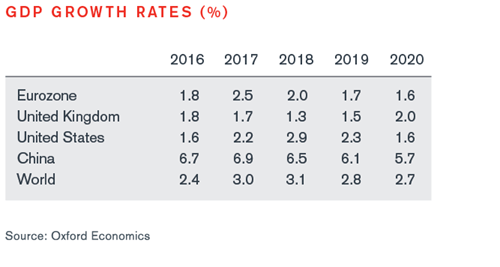

The uncertainties that were stressed in the last quarterly note continue to dominate the economic outlook. The world’s two largest economies, the United States and China, are still growing rapidly, but the trade war that America has declared and that China has, grudgingly, taken on, will have negative effects on their future prospects. Emerging markets, on the other hand, are slowing down almost everywhere, with the notable exception of India. As for Europe, it is uneasily poised between a continuation of steady, if unspectacular, growth and a plunge into much slower developments.

The United States are still benefiting from earlier accommodating policies and from (an ill-timed) fiscal stimulus. Confidence is high, Wall Street is at record levels and higher interest rates have, so far at least, hardly impinged on economic growth. China is also growing solidly, helped by some monetary relaxation. Both countries will, however, suffer from their trade conflict. Given the trade imbalance, China is more at risk, but America too will feel the effects of higher domestic prices because of its tariffs and of lower exports because of Chinese tariffs. Rough estimates by Oxford Economics suggest that US growth could be up to ½ a percentage point lower in 2019 because of protectionism. The effect on China would be somewhat higher.

The emerging world (outside China) is suffering from a strengthening dollar and higher US interest rates. Dollar denominated debt had increased rapidly in the last few years and this is now weighing on these countries’ currencies and growth. Argentina and Turkey are extreme examples, magnified by bad policy communications in one case and by an inappropriate policy stance (at least until recently) in the other. But pressures have also increased on the “five Rs” currencies: the South African rand, the Brazilian real, the Russian rouble, the Indian rupee and the Indonesian rupiah. In many of these countries, monetary policy has moved into a restrictive direction. And falling commodity prices add to the gloom. Among the major economies, only India is still keeping up its growth momentum.

Europe continues to enjoy reasonable growth rates. This is particularly true of Eastern Europe. Forecasts for the Czech Republic, Hungary and Poland, for instance, have been revised upwards in the last few months (rather than downwards as in Western Europe). And even the U.K. has seen some modest strengthening of activity. The main danger facing Britain is a stalemate in the Brexit negotiations and, therefore, an abrupt, non-consensual break with the European Union. Hopefully, this will be avoided as it is not in the interest of either partner, but should it happen, UK growth in 2019-20, presently put at a cumulative 3½ per cent, could well be curtailed by some 2 percentage points, or even more. Britain, in other words, would face virtual stagnation for at least two years.

For the rest of Europe the effects of an acrimonious Brexit would be much smaller, with the exception of Ireland. Irish growth over the next two years, presently put at some 2½ per cent per annum, could be reduced by 1½ percentage points of GDP. In the four major Continental countries (Germany, France, Italy and Spain), the output loss generated by a “hard” Brexit would, however, be limited to a quarter percentage point of GDP at most, with marginally higher costs for Greece and Belgium.

Assuming that the Brexit issue is, after all, resolved in an amicable way, the Euro area should continue to grow at a rate close to its potential, or between 1½ and 2 per cent per annum. Policies are still broadly accommodating, inflation is, very slowly, inching upwards, unemployment is declining and the euro has, for some time now, been relatively stable at a level that looks comfortable. Spain, which has been virtually untouched so far by the Catalonian controversy, remains the fastest grower, followed by France and Germany, while Italy, as in the past, is the weakest link.

Confidence, however, is falling among both consumers and producers, particularly in the manufacturing sector. Some of this may well reflect the trade tensions in the world at large. The EU, though hit by tariffs on its steel and aluminium exports, was able to obtain an armistice with the United States as far as further protectionist moves go. But it is only an armistice and the armistice does not cover trade in automotive equipment. Given Trump’s unpredictability (and his often expressed threats against Germany’s car exports), the danger of escalation is always present. A second potential danger comes from oil prices. These have already risen by some 50 per cent over the last year and could rise further after 1st November when US sanctions against Iran come into place. In addition, the European Central Bank is beginning to cut down on its quantitative easing. Positive short-term interest rates are only expected to materialize in the second half of 2019, but longer-term interest rates are rising already. While an increasing spread between short and long rates gives more breathing space to the banking sector, it would also put some pressure on often over-indebted households, corporations and even governments.

Europe’s other worry, as mentioned in the last quarterly note, is the spread of populism. This makes it much more difficult to enact the necessary reforms of the euro area’s institutional framework and could also lead to counterproductive fiscal policy expansions. Such a fear is particularly pronounced in the case of Italy. Despite the Italian government’s earlier assurances that the EU’s imposed limits on the budget deficit would be respected, the latest plans foresee a sharp rise in the deficit for 2019 to 2021. This is already leading to higher long-term interest rates which would, in turn, undo some of the hoped for expansionary effects of fiscal expansion. There is also the danger of a conflict with Brussels whose outcome it is very difficult to predict. Financial market confidence could decline, thus further endangering the Eurozone’s relatively modest prospects.

Duff & Phelps expressly disclaims any liability, of any type, including direct, indirect, incidental, special or consequential damages arising from or relating to the use of this material or any errors or omissions that may be contained herein.

Valuation Services

When companies require an objective and independent assessment of value, they look to Kroll.

Real Estate Advisory Group

Leading provider of real estate valuation and consulting for investments and transactions.