Tue, Mar 26, 2019

The Current State(s) of Wayfair: Tracking the New Nexus Laws Across the Country

Download the Report

The South Dakota v. Wayfair1 ruling has frantically ushered in a whole new era for sales and use tax laws and the end of an era for online shoppers reaping the benefits of untaxed purchases. Now, it’s time to step back, take a deep breath and assess just where things stand on a state-by-state basis. In what is now the post-Wayfair world, interpretations and customization of the new economic nexus requirements have started to emerge across states, and remote sellers need to maintain a watchful eye on how the changes can significantly impact their business.

As we chronicled previously, the 1992 U.S. Supreme Court ruling in Quill Corp. v. North Dakota2 had what some might call a stranglehold on state and local tax revenues for almost 30 years by deciding that out-of-state sellers must have a physical presence in a state before sales tax collection laws could be imposed. With Wayfair, however, the Court caught up with modern times and overturned this precedent in June 2018 when it ruled that physical presence was no longer required.

Case closed, right? Not exactly. In their ruling, the Supreme Court, somewhat intentionally, left considerable uncertainty on how the states, and in turn, merchants, should respond to elimination of the long-standing physical presence standard. Moreover, with no legislation from Congress yet3, technically, there’s no judicial or federal guidance on creating a uniform approach to the new economic or virtual nexus rules. Add in the fact that 45 states and more than 10,000 local, county and district sales tax jurisdictions are in play, it’s easy to understand why many taxpayers are a bit perplexed regarding how (and when) to best implement uniform policies and procedures regarding the collection and remittance of sales/use tax.

So, here we stand just shy of one year since the Wayfair ruling with even greater prospect for conflicting interpretation between courts, states and taxpayers. Whether Congress will be able to pass any meaningful legislation is still anybody’s guess, which means taxpayers, tax collectors and tax practitioners are on their own to figure things out. Meaning, if you thought the interstate collection of sales taxes from remote sellers was going to get easier following the Wayfair decision, think again. And if you thought any decision from federal lawmakers on how to address the issue would be immediately forthcoming, think again…again.

It’s Not Just for Online Sellers Anymore

One thing we need to make clear upfront – and something that seemed to get lost in the Wayfair fanfare – is the fact that the ruling extends to all companies, not just online retailers and not just domestic companies. Over and over, media coverage correlated the case exclusively to online businesses, so much so that “remote” sellers became synonymous with online sellers. But remote sellers cover a wide spectrum of business concerns outside the realm of the internet, and all businesses need to assess their exposure to the possibility of new tax rules.

For example, if your business deals with any of the following transactions, you’ll need to determine whether the economic or virtual nexus rules apply and, if so, how:

- Drop shipments

- Intercompany transactions

- International sellers (no physical presence in the U.S.)

- Software as a service (SaaS) and/or software license agreement (SLA)

- Services (e.g., information services)

- Wholesales (most thresholds relate to gross sales, not just taxable sales)

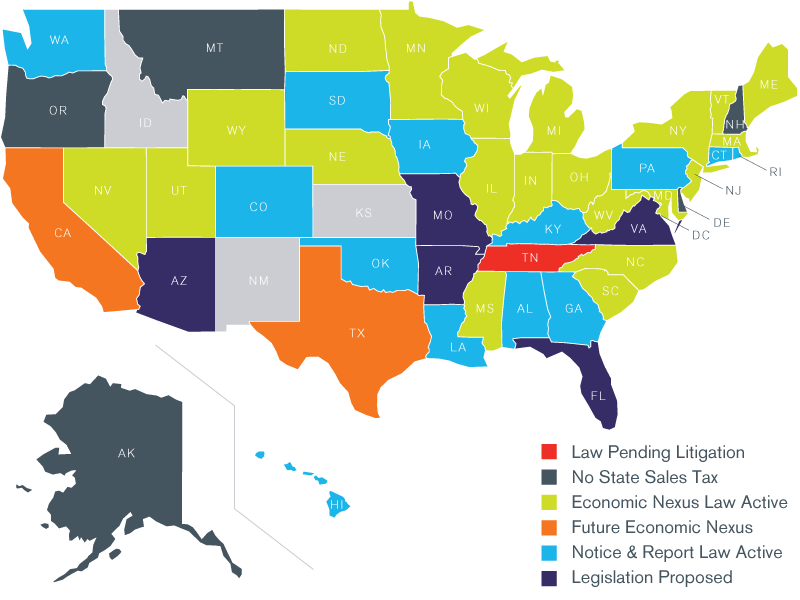

South Dakota Leads the Way

Since the Wayfair ruling, states have been looking for ways to impose their sales tax laws, with many tweaking their existing laws to establish “economic presence” thresholds that define when an out-of-state company is subject to their state’s sales tax collection responsibilities. Others are simply adopting rules through the issuance of administrative guidance. In either case, companies everywhere are facing a multitude of new filing requirements.

While the Supreme Court stopped short of upholding South Dakota’s law as being constitutional, it strongly suggested that following “the Wayfair checklist” would pass constitutional muster and offered several reasons why the state’s law and its tax compliance system would not be a burden on interstate commerce.

Most agree that the South Dakota law makes sense. In fact, many states have already adopted laws either identical or very similar, including:

- An economic nexus threshold of $100,000 in annual sales or 200 annual transactions

- The rejection of retroactive enforcement

- Membership in the Streamlined Sales Use Tax Agreement4

Since the Court didn’t officially rule on the validity of South Dakota’s law and no uniform federal law has been put in place, dozens of states are passing their own customized versions of the law or are enforcing existing nexus laws and rules they already had on the books.

Colorado, Hawaii and Illinois have adopted sales tax changes similar to South Dakota’s, but other states are taking a slightly different approach. Alabama, for example, is among the states that implemented a higher threshold so that retailers and marketplace facilitators must collect and remit sales tax when they have sales in excess of $250,000 with in-state customers. Georgia’s sales thresholds are also $250,000 or 200 or more retail sales with Georgia residents.5

In Washington, if an out-of-state company makes sales in the state of at least $100,000 or 200 transactions in the current or prior year, the company must collect and remit sales tax. However, if the company has less than $100,000 or 200 transactions for purposes of collection, but its sales exceed $10,000, the company has the choice to register and collect the sales tax or follow certain use tax notice and reporting requirements.6 Pennsylvania also has a $10,000 registration or collection threshold that went into effect on April 1, 2018.7

States that implemented sales tax thresholds have had different effective dates for their changes, as well. Hawaii’s changes were effective immediately, July 1, 20188, while Illinois’s changes took effect October 1, 20189 and Colorado’s on December 1, 2018.10 Although nearly half of the states’ changes went into effect in 2018, a few took effect for the first time in 2019. Six states, including Utah, had sales tax changes that took effect on January 1, 2019.11 California has changes effective April 1, 2019.12 Pennsylvania’s $100,000 mandatory collection requirement comes into effect July 1, 2019.13 Of the states that have not adopted economic nexus standards, over half introduced legislation to do so, while just a few states have yet to make any changes to their sales tax processes, including Idaho, Kansas and New Mexico. The list goes on.

Navigating Economic Nexus Laws in a Post-Wayfair Landscape

Will Congress Get on Board?

There hasn’t been a lot of traction at the federal level around establishing uniform sales tax rules. While some simplification bills have been introduced at the federal level, Congress has been reluctant to pass legislation that impedes on the states’ ability to collect sales tax. Many feel that without the mandate of a federal bill, it will be extremely difficult to help remote sellers cope with new tax collection obligations.

However, the progress made by Congress shouldn’t be ignored. For example, Rep. Bob Gibbs (R-Ohio) introduced the Protecting Businesses from Burdensome Compliance Cost Act of 2018, designed to ease the burden for out-of-state vendors working to comply with sales and use taxes in other states. Remote sellers need to be aware of the provisions proposed in this bill, including:

- Legislation would establish a start date, not prior to January 1, 2020, for states to require collection and remittance of sales tax by out-of-state sellers.

- States cannot retroactively collect sales tax for previous interstate sales where no nexus existed.

- States that want to collect sales tax from out-of-state vendors who do not have a nexus must enact legislation that:

o Provides a statewide uniform tax rate that cannot be higher than the highest combined rate of all local and state taxes;

o Permits out-of-state vendors to remit sales taxes to one location; and

o Provides a statewide uniform provision for what is taxable. - Vendors that have nexus can operate as they currently do.

There’s a Lot of Moving Parts Here: Where Do I Start?

The Court’s ruling was clear in one aspect: physical presence was no longer the only determinant for collecting and remitting sales tax. However, it did not articulate a test for determining whether a retailer’s economic contacts with a state were enough to justify the imposition of taxes, saying only that the necessary nexus “is established when the taxpayer or collector avails itself of the substantial privilege of carrying on business in that jurisdiction.” That kind of language leaves a lot to the imagination.

The fact is, as a remote seller in today’s marketplace, you will need to be vigilant about keeping track of changes to tax rules, state-by-state. Always be cognizant of the following:

- Most large companies will find they are required to register and collect tax in additional states.

- Sales tax is administered at the legal entity level, potentially leading to the required registration and filing by multiple subsidiaries.

- Foreign entities with no domestic presence are now drawn into the web of registering and reporting.

- Documentation supporting non-taxable sales will be required for each entity meeting the thresholds.

- Nearly all states base the nexus thresholds on gross sales, so even wholesalers are required to register when all sales are exempt.

- Entities “conducting business” in a state without the required permits are subject to civil and criminal penalties.

- Companies will still be required to determine on a state-by-state basis what goods and services are subject to tax, including B2B and B2C digital goods and services provided over the web.

And, be prepared to consider your economic ties to each state:

- Determine where the transaction is sourced.

o This may be especially difficult in drop shipment scenarios where ultimate consumer location may be unknown.

o Electronic downloading of software, SaaS, cloud computing and other services with multiple benefit locations complicate the sourcing of tax. - States have differing rules for sourcing sales.

o Delivery of sale or service (even where a report is delivered when a service is provided in a different location)

o Where the benefit of the service is received

o Billing address of the customer - Determine whether Wayfair nexus rules are applicable.

- Be aware of sales dollar and transaction volume activity.

- Consider your jurisdictions and whether there are prior period obligations and/or effective dates.

- Be prepared to track which jurisdiction has the strongest claim on any tax due.

- Decide which jurisdiction has priority: where the service is performed, or where the service is received (if both states tax the service provided, they could both attempt to tax the transaction).

- Assess the risk of overpaying tax where you are accruing use tax – many vendors may start taxing items as a result of now having nexus.

- Where the company is not a direct retailer, determine who is ultimately responsible for the collection of tax.

Case Study: Learning by Example

Now that Wayfair is the law of the land, how can you be affected by the new economic and virtual nexus laws and determine if you are liable to pay sales tax in a particular state? It’s certainly a tangled web right now. We know that physical presence is no longer the deciding factor, so looking at the places where you’ve physically conducted business (where your warehouse is, where you’ve been a vendor, etc.) is no longer the sole litmus test. While the exact requirements of each state’s law vary, the impact on your business is the same: you must now figure out where you are liable to pay state sales tax and then take steps to comply with the applicable sales tax laws.

For example, consider a multi-national company that is primarily a manufacturer and wholesaler. It has historically been filing in approximately a handful (ten) of states where it maintained sales offices, employees and warehouses for one domestic company, while also operating a foreign manufacturing entity that makes direct sales and shipments to retailers in the U.S.

Here’s how the new nexus laws affect their operations:

- Because they had acquired small retail operations making internet sales, tax is now required to be collected in those jurisdictions where the historic entity has a physical presence.

- Newly issued economic nexus guidelines have added approximately 25 new states that the domestic company will be required to register, collect and file for, including collection for retail sales now in 35 states.

- Additionally, the foreign manufacturing entity is now required to also register in approximately 35 states.

- Both entities are now required to obtain resale documentation to support non-taxable sales in each state or risk being assessed under audit.

- The firm conducting the financial audit requested this information, so it is something that companies cannot ignore.

Stating the obvious, because of Wayfair and its aftermath, many companies that had little to no sales/use tax exposure find themselves with a monumental compliance burden, and significant cost in the form of interest and penalties as well as liability for tax if unpaid by their customer in event of an examination.

Finding Help to Solve the Puzzle

There is no easy answer to the consequences of Wayfair and it is very unlikely Congress will act to pass legislation that provides uniform standards. Seeing how quickly most states have reacted to the ruling, it would be prudent to anticipate that the states will become even more aggressive in auditing compliance with the new remote seller registration and collection requirements.

We anticipate additional state activity in 2019 around the sales tax issue, particularly among those that adopted a wait-and-see-approach after the Wayfair decision. Companies will need to work through the ramifications of widely varying sales tax law changes, including how to tackle the state registration process, how to ensure collections are both collected and remitted, and which transactions may be eligible for a sales tax exemption. Companies face a myriad of priorities operating in a post-Wayfair world, including:

- Software applications can help, but no software system can correctly source and properly tax all transactions at this time.

- Consider whether to outsource/co-source some of the sales tax functions where internal resources are inadequate.

- Proper planning may allow companies to mitigate additional compliance costs (e.g. procurement company).

For more information on how you can prepare for changes in state and local tax collection obligations on remote and online vendors, please contact Duff & Phelps Sales and Use Tax experts.

Sources:

1 South Dakota v. Wayfair, Inc., U.S. S. Ct. Dkt No. 17–494, 6/21/2018

2 Quill Corp. v. North Dakota, 504 U.S. 298 (1992)

3 On March 13, 2019 both houses of Congress have introduced legislation as another attempt to simplify the taxation of digital goods and services and promote fairness. Similar versions have failed in past sessions of Congress. The Digital Goods and Services Tax Fairness Act of 2019, if passed will establish rules for sourcing of digital goods and services to the home state of the consumer. This would simplify the taxation of digital goods and services such as downloading of software or music and eliminate the claim by multiple states on a transaction. While this would help both consumers being taxed more than once on the same transaction and help vendors know which tax should apply, it misses the overall mark of addressing many of the difficulties resulting from the Wayfair decision. (See https://www.thune.senate.gov/public/_cache/files/0d6ea608-a152-41f8-b617-1321cf4230b2/2989ACD9D31B430D694A6C26C8C995FE.03-13-19-dgstfa-1-pager-final.pdf)

4 CA, CO, DC, HI, IL, IN, IA, KY, LA, ME, MD, MI, NE, NV, NJ, NC, ND, RI, SD, UT, VT, WA, WV, WI, and WY have all adopted the $200,00 annual gross sales or 200 transaction thresholds for economic nexus.

5 Ga. Code Ann. § 48-8-2 (M.1-M.2)

6 Washington Guidance https://dor.wa.gov/find-taxes-rates/retail-sales-tax/marketplace-fairness-leveling-playing-field/registration-thresholds-out-state-businesses-retail-sales; Emergency Rule RCW 34.05.350 amending WAC 458-20-193 and 458-20-221

7 Pa. Stat. Ann. § 7213.1(a)

8 Haw. Rev. Stat. § 237-2.5

9 Ill. Admin. Code 150.803

10 News Release: Colorado to require online retailers to collect sales tax, Colo Dep't. Rev., 09/11/2018

11 Utah Code Ann. § 59-12-107(2)(c)

12 California Department of Tax and Fee Administration News Release NR 59-18, 12/11/2018

13 id

Tax Services

Built upon the foundation of its renowned valuation business, Kroll's Tax Service practice follows a detailed and responsive approach to capturing value for clients.

Sales and Use Tax Services

Kroll provides a comprehensive suite of sales and use tax services to assist companies in complying with its sales and use tax obligations.